Let’s be honest, the very idea of discussing term life insurance for seniors UK can feel a bit… well, daunting, right? It’s often viewed as something you sort out in your younger years, then forget about. But here’s the thing: life doesn’t stop, and neither do our responsibilities or our desire to provide for our loved ones, no matter our age. If you’re a senior in the UK, perhaps you’ve wondered if it’s even possible to get a decent policy, or if it’s just too expensive. Maybe you’ve heard myths that make it seem out of reach. Well, pull up a chair, because I’m here to tell you that not only is it possible, but with the right approach, it can offer incredible peace of mind . This isn’t just about reporting facts; it’s about guiding you through the often-confusing landscape of life insurance, specifically tailored for life insurance for older people in the UK.

My goal today? To cut through the jargon, bust some myths, and give you a clear, actionable roadmap. Think of me as your personal guide, helping you understand how to secure that vital financial safety net, even if you’re in your golden years. We’re going to explore what makes term life insurance for seniors UK a viable option, how to navigate the application process, and most importantly, how to find a policy that genuinely fits your unique circumstances and budget. Because ensuring your family’s future, even for things like funeral cover UK , is a conversation worth having, and a plan worth making.

Why Even Consider Term Life Insurance for Seniors UK? It’s More Than Just a Policy

You might be thinking, “I’m retired, my kids are grown, why do I still need life insurance?” And that’s a perfectly valid question. But the truth is, financial obligations don’t always disappear with retirement. Perhaps you have outstanding mortgage debt, or you want to ensure your partner is financially secure should you pass away. Maybe you want to leave a small inheritance, cover potential inheritance tax, or simply ensure your funeral costs don’t become a burden on your family. This is where term life insurance for seniors UK truly shines. It’s not about getting rich; it’s about thoughtful planning and preventing financial strain on those you care about most.

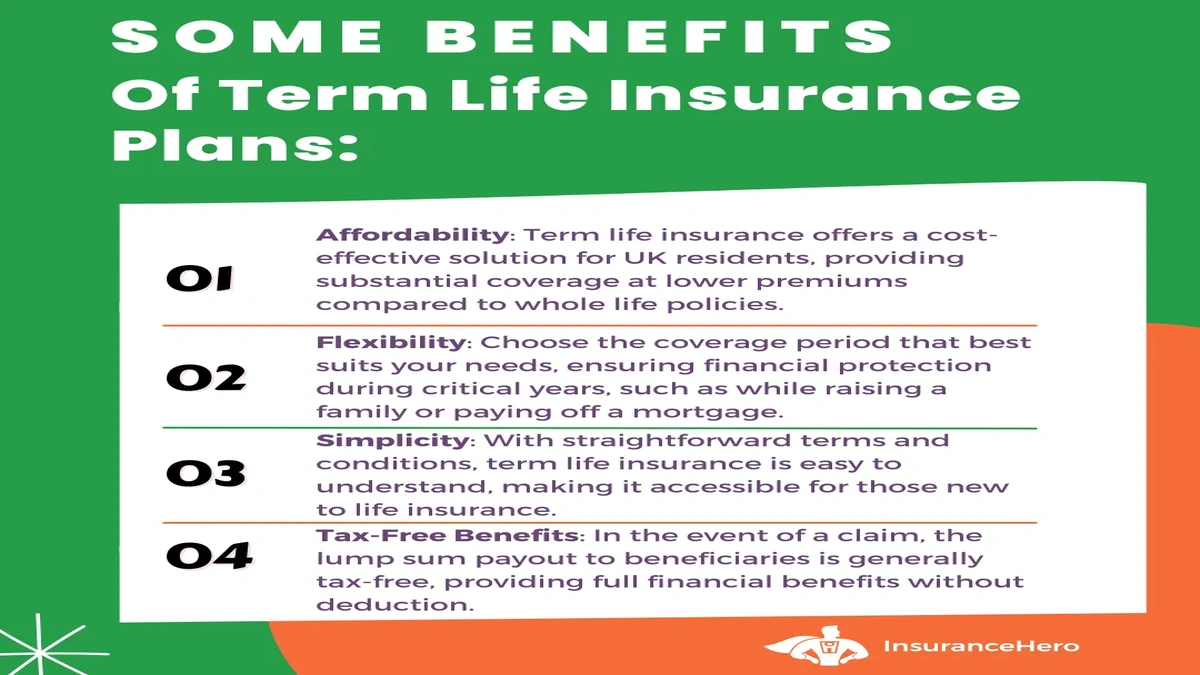

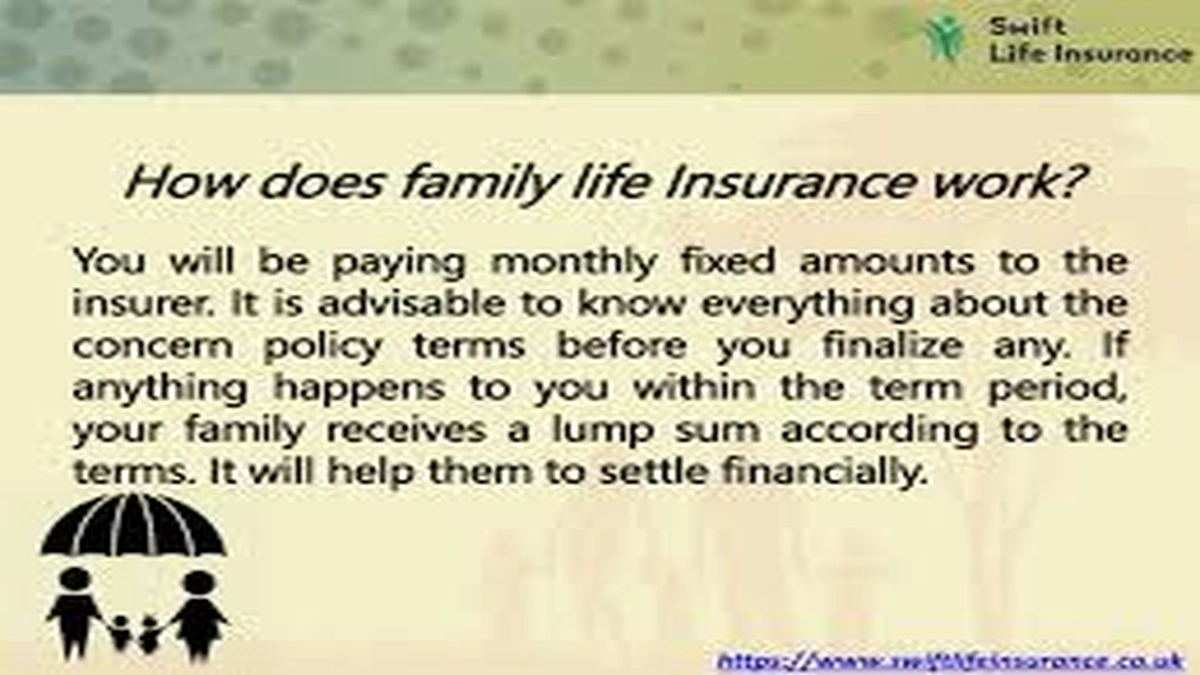

Unlike whole life insurance , which covers you for your entire life and often has an investment component, term life insurance is designed to cover you for a specific period – a ‘term’ – say, 10, 15, or 20 years. If you pass away within that policy term , your beneficiaries receive a pre-agreed sum assured . If you outlive the term, the policy simply ends, and you don’t get anything back. While that might sound unappealing, it’s precisely why term policies are often more affordable life insurance UK options, especially for seniors. It allows you to tailor coverage to a specific need or timeframe, like covering the remaining years of a mortgage or until a grandchild finishes university. For many looking for life insurance over 70 UK , this focused approach can be incredibly practical and cost-effective.

Decoding Your Options | What Kind of Term Life Insurance Fits You?

Alright, so you’re on board with the ‘why.’ Now for the ‘how’ of choosing. The UK life insurance market offers a few flavours of term life insurance, and understanding them is key to finding the best life insurance for seniors UK . The two main types are:

- Level Term Insurance: With this, the sum assured (the payout) remains the same throughout the entire policy term . So, if you take out a £50,000 policy for 10 years, your beneficiaries will receive £50,000 whether you pass away in year one or year nine. This is great if you have a specific financial goal, like leaving a fixed amount to cover inheritance tax or a lump sum for your family.

- Decreasing Term Insurance: Here, the sum assured gradually reduces over the policy term . This type is often linked to a repayment mortgage, where the amount paid out decreases as your mortgage balance goes down. It’s generally the most affordable life insurance UK option because the risk to the insurer decreases over time. If your primary concern is covering a specific debt that reduces over time, this could be a smart choice.

When considering options like over 50s life insurance UK , you’ll find that many policies are specifically designed for older applicants, sometimes with simpler application processes. The premiums, of course, will depend on several factors: your age, the length of the term, the sum assured , and crucially, your health. This brings us to the next big hurdle for many seniors.

The Application Journey | Navigating Medical Questions and “No Medical Exam” Policies

This is often where the worry creeps in. “I’m older, I have a few health conditions, surely no one will insure me?” This is a common misconception! While it’s true that age and health play a significant role in determining premiums, it doesn’t automatically disqualify you. Insurers assess risk, and they do this by asking medical questions about your current health, medical history, and lifestyle (do you smoke? How much do you drink?).

For some, a full medical exam might be required, but often, it’s just a detailed questionnaire. Be completely honest; withholding information can invalidate your policy later. If you have conditions like diabetes or high blood pressure, it doesn’t mean you can’t get cover, but it might mean slightly higher premiums. The key is to shop around, as different insurers have different appetites for risk and may offer better terms for specific conditions.

Now, what about no medical exam life insurance UK ? This is a popular option, especially for seniors. These policies, often marketed as ‘guaranteed acceptance’ or ‘over 50s plans,’ typically don’t require you to answer detailed health questions or undergo an exam. Sounds great, right? It often is, but there’s a trade-off. The sum assured is usually lower, and the premiums can be higher compared to a fully underwritten policy. There’s also often a ‘waiting period’ (typically 1-2 years) during which, if you pass away from natural causes, your beneficiaries might only receive back the premiums paid, not the full sum assured . However, if your primary goal is to ensure funeral cover UK or leave a modest sum without the hassle of medical checks, these can be an excellent, straightforward solution.

Beyond the Basics | Important Considerations and Add-ons

Once you’re looking at specific policies, it’s worth considering a few extra layers of protection. While term life insurance focuses on a payout upon death, some policies offer add-ons or can be combined with other types of cover:

- Critical Illness Cover UK: This isn’t technically part of your life insurance payout, but it’s often offered alongside it. It pays out a lump sum if you’re diagnosed with a specified critical illness (like a heart attack, stroke, or certain cancers) during the policy term . This can be invaluable for covering medical costs, adapting your home, or providing income protection if you’re still working or your partner needs to take time off to care for you.

- Reviewing Existing Policies: Before jumping into a new policy, take a moment to review any existing life insurance or death-in-service benefits you might have through former employers or previous policies. You might have more cover than you think, or perhaps your needs have changed, and a new policy can top up or replace an older, less suitable one. This is a crucial step in building comprehensivebest life insurance policyfor your overall financial plan.

Remember, the goal is financial security for your loved ones. Don’t just think about the immediate payout; consider the broader financial landscape your family might face.

Finding Your Perfect Policy | Tips for Comparing and Choosing

Navigating the various options can feel like a maze, but there are clear paths to finding the right term life insurance for seniors UK . Here’s my advice:

- Know Your Needs: Be crystal clear about why you want the insurance. Is it to cover a specific debt? Leave an inheritance? Pay for your funeral? The clearer you are, the easier it will be to choose the right type and sum assured .

- Use Comparison Websites: Websites like MoneySuperMarket, Compare the Market, or Confused.com are excellent starting points. They allow you to input your details and get quotes from multiple insurers quickly. Just remember, they don’t always cover every provider, especially specialist ones.

- Consider a Financial Advisor: For more complex situations, or if you simply prefer personalized advice, an independent financial advisor specializing in insurance can be invaluable. They can assess your unique situation, recommend suitable policies, and even help you navigate the application process. They often have access to policies not available directly to the public.

- Read the Small Print: I know, I know, it’s tedious. But it’s vital. Understand the exclusions, the exact terms, and what happens if you miss a payment. Don’t be afraid to ask questions until you’re completely clear. For general advice on managing finances in the UK, a great resource is the government-backedMoneyHelper website.

- Don’t Be Afraid to Re-evaluate: Life changes. Your health might improve, debts might be paid off, or new responsibilities might emerge. Periodically review your policy to ensure it still meets your needs. For instance, if you’re a small business owner, your needs might evolve, much like understandingcommercial insurance for small business India guide.

Ultimately, securing term life insurance for seniors UK isn’t about finding the cheapest option; it’s about finding the right option that provides genuine financial security and peace of mind for you and your loved ones. It’s an act of love and foresight, ensuring your legacy is one of care and responsibility.

Frequently Asked Questions About Term Life Insurance for Seniors UK

Can I get term life insurance if I’m over 70 in the UK?

Yes, absolutely! While premiums may be higher than for younger individuals, many insurers in the UK life insurance market offer policies for those over 70, and even over 80. Options like ‘over 50s plans’ or ‘guaranteed acceptance’ policies are specifically designed for older applicants, often without extensive medical questions .

Is a medical exam always required for senior life insurance?

Not always. While some policies, especially those with higher sum assured , might require one, many ‘guaranteed acceptance’ or ‘over 50s life insurance UK’ policies do not. These are specifically tailored to provide cover without a medical exam, though they might have lower payouts or a waiting period.

What’s the difference between ‘term’ and ‘whole’ life insurance for seniors?

Term life insurance for seniors UK covers you for a specific period (e.g., 10-20 years) and pays out only if you pass away within that policy term . Whole life insurance covers you for your entire life, regardless of when you pass, and usually has a savings or investment component. Term policies are generally more affordable but don’t pay out if you outlive the term.

How can I make term life insurance more affordable as a senior?

Consider decreasing term policies if you’re covering a diminishing debt like a mortgage. Opt for a shorter policy term if your needs are specific and time-bound. Also, explore ‘over 50s plans’ for potentially more accessible (though often lower sum assured ) options. Shopping around and comparing quotes from multiple providers is also key to finding affordable life insurance UK .

What if I have pre-existing health conditions?

Having pre-existing conditions doesn’t stop you from getting life insurance. You’ll need to disclose them during the application. Insurers will assess the risk, and while your premiums might be higher, many policies are still available. For serious conditions, ‘guaranteed acceptance’ policies might be a viable, albeit lower-coverage, option.

Can I use term life insurance to cover funeral costs?

Yes, many seniors choose term life insurance for seniors UK specifically to cover their funeral cover UK costs, preventing this financial burden from falling on their family. ‘Over 50s plans’ are particularly popular for this purpose due to their straightforward application process.