Let’s be honest, trying to understand the private health insurance UK cost per month can feel like deciphering ancient hieroglyphs. You see numbers, you get quotes, but do you really grasp why that specific figure lands in your inbox? It’s not just about paying for a service; it’s about making an informed decision for your health and your wallet in the complex landscape of the UK healthcare system. And frankly, it’s a decision that’s becoming more critical for many across the nation.

I’ve seen countless people get caught up in the ‘what’ of private health insurance – what does it cover, what’s the cheapest option? But what truly fascinates me, and what I believe is far more valuable for you, is understanding the ‘why’. Why do premiums vary so wildly? Why is your friend paying less than you for seemingly similar cover? This isn’t just about finding a good deal; it’s about understanding the underlying mechanics so you can genuinely compare private health insurance UK options and secure peace of mind, not just a policy.

The truth is, the average cost of private health insurance UK isn’t a single, static number. It’s a dynamic figure, a blend of personal circumstances, policy choices, and the broader economic climate. So, let’s peel back the layers and truly understand what’s going on.

Beyond the Sticker Price | What Really Drives Your UK Private Medical Insurance Premiums?

When you get a quote for your UK private medical insurance premiums, it’s not just a random figure pulled from thin air. Insurers, much like any business assessing risk, look at a multitude of factors to determine how likely you are to claim and how expensive those claims might be. It’s a sophisticated calculation, and understanding these elements is your first step to taking control.

Age, Location, and Lifestyle | The Personal Equation

It sounds obvious, but your age is a massive factor. Generally, the older you are, the higher your insurance premiums will be. Why? Because the likelihood of needing medical treatment increases with age. Similarly, where you live can influence costs. If you’re in an area with higher private hospital charges or a greater concentration of specialists, your premiums might reflect that. Lifestyle choices, too, play a part – smoking, for instance, is a known risk factor that can push costs up. It’s the insurer’s way of balancing their books against the potential costs of your future health needs.

Your Medical History and the Underwriting Process

This is where things get a bit more personal. Most policies involve an underwriting process. This means the insurer will look at your past and current health conditions. If you have pre-existing conditions, these might be excluded from your cover, or your premiums might be adjusted to reflect the increased risk. It’s a crucial aspect that often surprises people. I’ve seen many assume all their existing ailments will be covered, only to find out post-purchase that their chronic back pain, for example, isn’t included. Always, always be transparent about your medical history to avoid issues later.

Policy Choices | Excess, Outpatient Limits, and Hospital Networks

This is where you have the most direct control. The ‘excess’ is the amount you agree to pay towards a claim before your insurer steps in. A higher excess typically means lower monthly premiums. Makes sense, right? You’re taking on more of the initial risk. Then there are outpatient limits – some policies offer full outpatient cover, others limit it, and some exclude it entirely. This impacts the private health insurance UK cost per month significantly. And finally, the hospital network: opting for a more restricted network of hospitals can often lead to lower costs, as insurers negotiate better rates with specific providers. It’s a trade-off between choice and affordability, something we also consider when looking at options forcar insurance renewal online.

The NHS vs. Private Healthcare UK | Understanding the Value Proposition

Now, why would anyone even consider private health insurance when the NHS is, by and large, free at the point of use? This is the ‘why it matters’ question for many. It’s not about replacing the NHS; it’s about complementing it. The NHS vs private healthcare UK debate isn’t about one being inherently better, but about different priorities and needs.

Speed, Choice, and Comfort | The Private Healthcare Benefits UK

The primary drivers for choosing private healthcare are often speed of access, choice of specialist, and enhanced comfort during treatment. Waiting lists, especially for non-emergency procedures, can be long on the NHS. Private insurance offers the potential for quicker diagnosis and treatment, allowing you to get back to full health faster. You also often get to choose your consultant and schedule appointments at your convenience. And let’s not forget the amenities – private rooms, flexible visiting hours, and sometimes even better food can make a significant difference to the patient experience. This is where the private healthcare benefits UK truly shine for those who prioritise these aspects.

It’s worth noting that the NHS remains a cornerstone of our society, providing excellent emergency care and managing complex health conditions for millions. Private insurance is often about getting treatment for acute, curable conditions swiftly, allowing you to bypass some of the pressures on the public system. For a comprehensive overview of the NHS, you can visit the officialNHS website.

Navigating the Market | How to Compare Private Health Insurance UK and Find Value

Once you understand the ‘why’ behind the costs, the ‘how’ of finding the right policy becomes much clearer. The market is saturated with different health insurance providers UK, and each offers a myriad of policy variations. It can feel overwhelming, but a structured approach can save you both money and stress.

Getting Quotes and Understanding the Small Print

Don’t just jump at the first quote you see. Use reputable comparison websites (like MoneySuperMarket or ComparetheMarket in the UK, though always verify directly with the insurer) and get quotes from several providers. But here’s the crucial bit: don’t just look at the price. Dive into the policy documents. What exactly is covered? What are the exclusions? Are there any hidden clauses? The cheapest policy isn’t always the best value if it doesn’t cover what you need. This is particularly true when it comes to understanding the nuances of different types of coverage, similar to how one might carefully considerterm life insurance for seniors UK.

Considering Corporate vs. Individual Policies

Sometimes, your employer might offer a corporate health insurance scheme. These can often be significantly cheaper than individual policies because the risk is spread across a larger group. If this is an option for you, definitely explore it. If not, don’t despair; many excellent individual policies are available. The key is knowing what to look for and being prepared to ask questions.

Strategies to Manage Your Private Health Insurance Costs

So, you’re committed to private health insurance, but you want to keep that private health insurance UK cost per month in check. Good news: there are several strategies you can employ.

Increase Your Excess

As mentioned, opting for a higher excess is a direct way to reduce your monthly premiums. Just make sure the excess amount is something you could comfortably afford to pay if you needed to make a claim.

Consider a Six-Week Wait Option

Some policies offer a ‘six-week wait’ option. This means that if the NHS can provide your treatment within six weeks, you’ll use the NHS. If the wait is longer, your private insurance kicks in. This can significantly reduce your premiums, as it leverages the NHS for less urgent care.

Review Your Cover Annually

Your health needs change, and so does the market. Don’t just auto-renew your policy. Take the time each year to review your cover. Are you still happy with the benefits? Has your lifestyle changed? Could you get a better deal elsewhere? It’s a competitive market, and loyalty doesn’t always pay.

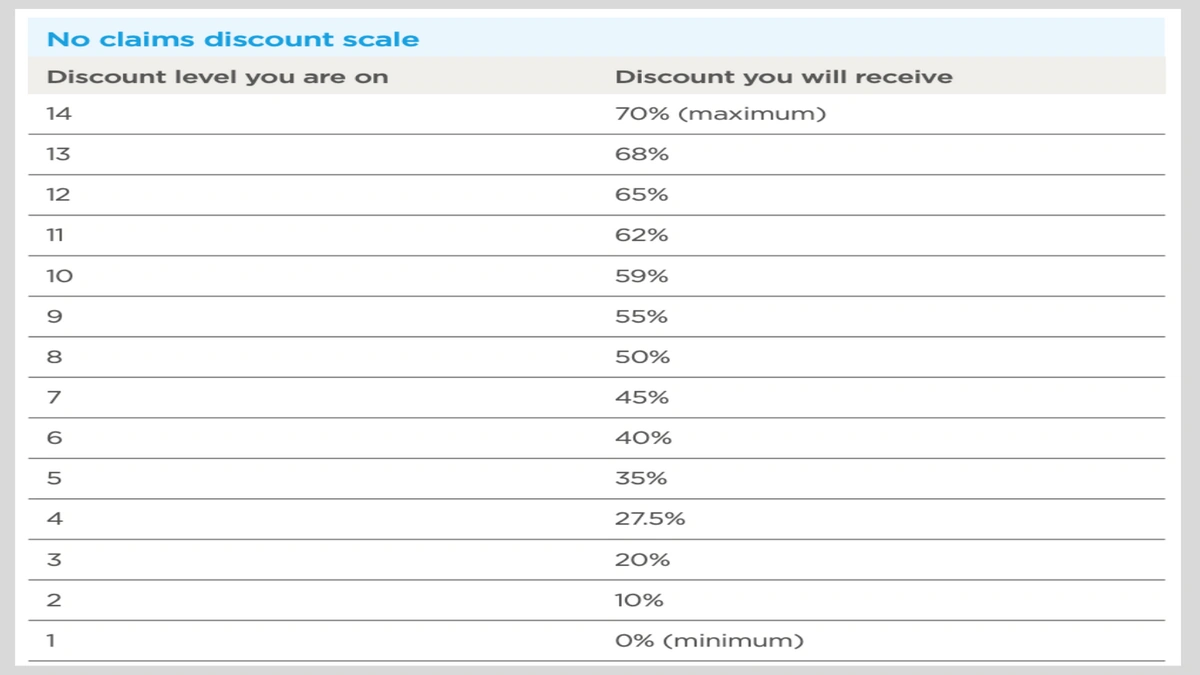

No-Claims Discount

Just like car insurance, some health insurance policies offer a no-claims discount. If you don’t claim for a certain period, your premiums can decrease. This is a nice bonus for those who maintain good health.

Pay Annually, Not Monthly

Many insurers offer a discount if you pay your premium annually rather than monthly. If you have the financial flexibility, this can be a simple way to save a bit of money over the year.

FAQ | Your Burning Questions About UK Private Health Insurance Costs Answered

Frequently Asked Questions About Private Health Insurance Costs

What is the average cost of private health insurance in the UK?

The average cost of private health insurance UK varies widely. For a young, healthy individual, it could be as low as £30-£50 per month. For older individuals or those with more comprehensive cover, it can easily exceed £100-£200 per month. It truly depends on age, location, chosen excess, and the level of cover.

Can I get private health insurance with a pre-existing condition?

Yes, it’s possible, but it might affect your cover. Many insurers will exclude the pre-existing condition from your policy, or they might offer ‘moratorium’ underwriting, where the condition might become covered after a certain period (e.g., two years) if you haven’t needed treatment for it. Always disclose everything upfront.

Is private health insurance worth the cost in the UK?

Whether it’s ‘worth it’ is a personal decision. For many, the peace of mind, quicker access to specialists, and choice of hospital and consultant justify the private health insurance UK cost per month. For others, the NHS meets all their needs. It’s about weighing your priorities against the financial outlay.

How can I reduce my private health insurance premiums?

You can reduce premiums by opting for a higher excess, choosing a more restricted hospital network, selecting a policy with less comprehensive outpatient cover, or considering a six-week wait option. Paying annually instead of monthly can also offer a small discount.

Do all private health insurance policies cover mental health?

Not always fully. While many policies now offer some level of mental health support, the extent of cover can vary significantly. Some might offer limited outpatient counselling, while others provide inpatient psychiatric care. It’s crucial to check the specifics of any policy if mental health cover is a priority for you.

The Bottom Line | An Investment in Your Wellbeing

Understanding the private health insurance UK cost per month is more than just knowing a number; it’s about grasping the intricate factors that shape that figure. It’s about being an informed consumer, not just a recipient of a quote. Private medical insurance is an investment in your health, your time, and your peace of mind. By understanding the ‘why’ behind the premiums, the benefits, and the strategies to manage costs, you’re not just buying a policy – you’re making a conscious decision about your future wellbeing. And that, my friend, is a decision worth making with clarity and confidence.