So, you’ve taken the plunge and started an LLC in the USA. Congratulations! That’s a huge step. But now, let’s talk about something less glamorous, yet absolutely crucial: general liability insurance for LLC USA cost. I get it, insurance can feel like wading through quicksand confusing, a bit scary, and often, you just want to know the bottom line: how much is this going to set me back?

Here’s the thing: while there’s no one-size-fits-all answer, understanding the factors that influence your commercial general liability premium isn’t as complex as it seems. Think of me as your friendly guide, helping you cut through the jargon and get to what truly matters. We’re going to break down the real cost, why it varies so much, and crucially, how you can get the best value without compromising your business’s safety net. Because let’s be honest, protecting your dream shouldn’t be a guessing game.

Why Your LLC Absolutely Needs General Liability Insurance (It’s Not Just a “Nice-to-Have”)

You might be thinking, “My LLC protects me, right?” And yes, an LLC offers personal asset protection. But here’s the crucial distinction: that protection doesn’t extend to the business itself if someone sues it for things like bodily injury or property damage. That’s where general liability insurance for LLC USA cost comes into play. It’s your first line of defense against common business risks.

Imagine this: a client slips and falls in your office, or a piece of your equipment accidentally damages a client’s property. Without adequate coverage, your business could face hefty legal fees, medical expenses, and settlement costs that could easily bankrupt even a thriving small business. This isn’t fear-mongering; it’s just the reality of doing business in the USA. Many clients or landlords will even require proof of this coverage before they’ll work with you, making it one of those essentialbusiness insurance policycomponents you simply can’t skip.

Unpacking the “How Much?” | Average Cost of General Liability Insurance

Alright, let’s get down to brass tacks. What’s the average cost of general liability insurance for an LLC in the USA? While it varies wildly, most small businesses can expect to pay anywhere from $300 to $1,000 per year for a basic general liability policy with a $1 million per-occurrence limit and a $2 million aggregate limit. Some very low-risk businesses might even find policies for as little as $200 annually, while higher-risk operations could easily pay $2,000 or more. See? It’s a spectrum.

But please, don’t just take that average and run with it. Your specific business is unique, and so will be its insurance needs and its small business insurance cost. Understanding the variables is key to getting an accurate quote and ensuring you’re not overpaying or, worse, underinsured. This is why getting personalized business liability insurance quotes is so important.

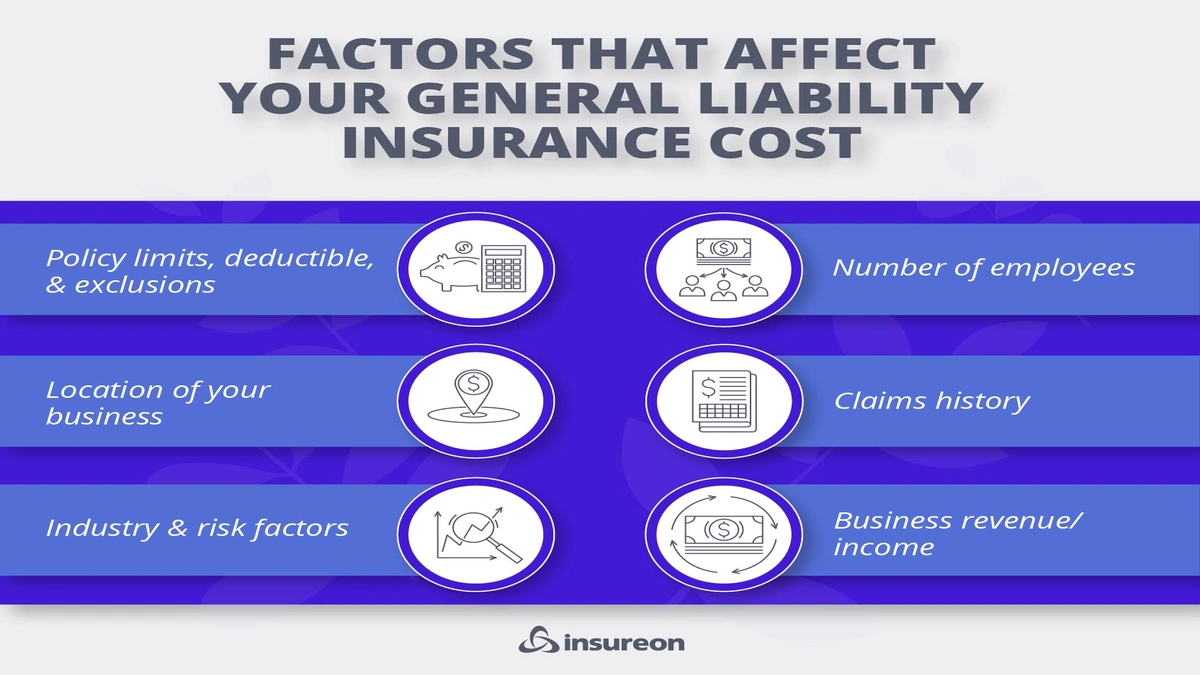

The Hidden Levers | Factors Affecting General Liability Insurance Costs

So, what makes one LLC pay $300 and another $2,000? It boils down to a few key factors affecting general liability insurance premiums. Let me walk you through them:

- Your Industry and Business Type: This is probably the biggest factor. A freelance graphic designer working from home faces far fewer risks than a construction company or a restaurant. Industries with higher potential for bodily injury or property damage claims (think physical labor, public interaction, or hazardous materials) will naturally have higher premiums. Insurers use NAICS or SIC codes to classify your business, so be accurate!

- Location, Location, Location: Where your LLC operates matters. Businesses in areas with higher population density, higher crime rates, or a history of more frequent lawsuits might see higher rates. State-specific regulations and local legal environments also play a role.

- Your Business Size and Revenue: Generally, the more employees you have and the higher your annual revenue, the more exposure you have to potential claims. More employees mean more potential for workplace incidents, and higher revenue often means more client interactions and larger projects, increasing the stakes.

- Coverage Limits and Deductibles: This is straightforward: higher coverage limits (e.g., $2 million per occurrence instead of $1 million) will increase your premium. Conversely, choosing a higher deductible (the amount you pay out-of-pocket before insurance kicks in) can lower your premium. It’s a balancing act: what level of risk are you comfortable retaining?

- Your Claims History: If your business has a history of previous general liability claims, insurers will see you as a higher risk, and your premiums will reflect that. A clean claims record is always a plus!

- Risk Management Practices: Do you have safety protocols in place? Employee training? Good record-keeping? Demonstrating proactive risk management can sometimes lead to lower rates, as it shows you’re actively trying to prevent incidents.

Understanding these variables is crucial. It’s not just about getting a cheap policy; it’s about getting the right policy for your unique LLC insurance requirements.

Navigating the Quote Process | How to Get the Best Deal (Without Cutting Corners)

Now that you know what influences the cost, how do you actually get a good deal? My advice is always to shop around. Don’t just go with the first quote you receive. Here’s a simple, actionable strategy:

- Gather Your Information: Before you start, have all your business details ready: business type, industry, number of employees, annual revenue, physical address, and any past claims history. The more accurate and complete your information, the more precise your quotes will be.

- Compare Multiple Providers: This is non-negotiable. Different insurance companies specialize in different industries or business sizes. What might be expensive with one insurer could be quite affordable with another. Use online aggregators, independent agents, or directly contact a few reputable insurers. Think about it like comparing life insurance premium calculator results; you wouldn’t just pick the first one, right?

- Understand Your Coverage: Don’t just look at the price tag. Read the policy details. What exactly is covered? What are the exclusions? Are there any endorsements you need (or don’t need)? A cheaper policy that doesn’t cover your specific risks isn’t a good deal at all. The U.S. Small Business Administration (SBA) offers great resources on understanding business insurance, which can be a useful external guide to types of business insurance.

- Consider Bundling: Many insurers offer discounts if you bundle multiple policies, such as general liability with commercial property insurance, professional liability, or a Business Owner’s Policy (BOP). A BOP is often a fantastic option for small to medium-sized businesses, combining general liability, commercial property, and business interruption insurance into one convenient, often cheaper, package.

- Ask About Discounts: Seriously, ask! Insurers often have discounts for things like having a security system, a clean claims history, being a member of certain professional organizations, or even paying your premium annually instead of monthly.

Remember, the goal isn’t necessarily the lowest general liability insurance for LLC USA cost, but the best value for your specific business needs. It’s about smart protection.

The Bottom Line | Investing in Peace of Mind

Ultimately, paying for general liability insurance for LLC USA cost is an investment in your peace of mind and the longevity of your business. It’s not an expense to be begrudged, but a fundamental safeguard that allows you to focus on what you do best: running and growing your LLC.

Don’t wait for a claim to realize you needed it. Take the time, do your research, get those business liability insurance quotes, and secure the protection your hard work deserves. Because when the unexpected happens and it often does you’ll be incredibly glad you did.

Frequently Asked Questions About LLC General Liability Insurance

What is the minimum general liability insurance coverage I should get?

While there’s no legal minimum in most states, a common starting point for small businesses is a policy with $1 million per-occurrence coverage and a $2 million aggregate limit. However, your specific industry, client contracts, and risk exposure might require higher limits. Always consult with an insurance professional to determine appropriate coverage for your unique LLC insurance requirements.

Can I get general liability insurance online?

Absolutely! Many reputable insurance providers and online brokers offer instant business liability insurance quotes and policies online. This can be a quick and convenient way to compare options and secure coverage, especially for straightforward, low-risk businesses.

Does general liability insurance cover professional mistakes?

No, general liability insurance typically covers claims of bodily injury, property damage, and advertising injury. It does NOT cover professional errors, negligence, or omissions in your services. For that, you would need professional liability insurance, also known as Errors & Omissions (E&O) insurance. It’s a crucial distinction for service-based LLCs.

Is general liability insurance legally required for an LLC in the USA?

In most U.S. states, general liability insurance is not legally mandated for all businesses. However, it is often required by client contracts, landlords, lenders, or licensing boards for specific industries. Even if not legally required, it is highly recommended for all LLCs to protect against common risks and potential lawsuits. Think of it as a practical necessity, not just an LLC insurance requirement.

How can I lower my general liability insurance cost?

You can potentially lower your general liability insurance for LLC USA cost by implementing strong risk management practices, choosing a higher deductible, bundling policies, maintaining a clean claims history, and shopping around with multiple insurers for competitive business liability insurance quotes. Also, ensure your business classification is accurate, as misclassification can lead to higher premiums.

What’s the difference between general liability and a Business Owner’s Policy (BOP)?

General liability insurance protects against third-party claims of bodily injury, property damage, and advertising injury. A Business Owner’s Policy (BOP) is a package policy that typically combines general liability insurance with commercial property insurance (covering your business’s physical assets) and often business interruption insurance (covering lost income due due to covered perils). For many small LLCs, a BOP offers more comprehensive coverage at a more affordable small business insurance cost than buying policies separately.