Let’s be honest, staring at that monthly bill for your family’s health insurance can feel like looking at a cryptic code, can’t it? You see a number, but you rarely understand the intricate dance of factors that led to it. It’s not just a premium; it’s a complex equation, influenced by everything from where you live to decisions made years ago in Washington D.C. What fascinates me is how many people pay this bill without truly grasping the ‘why’ behind their family health insurance monthly cost USA. And trust me, understanding that ‘why’ isn’t just academic; it’s empowering. It’s the difference between feeling helpless and making informed choices that could genuinely save your family thousands.

As someone who’s delved deep into the labyrinth of American healthcare financing, I can tell you this: the sticker price is rarely the whole story. We’re going to pull back the curtain today, exploring not just what you pay, but why you pay it, what hidden variables are at play, and crucially, how you can navigate this system more effectively. This isn’t just about reporting figures; it’s about giving you the analytical tools to genuinely understand your family’s healthcare spend. Because when you understand the game, you can play it smarter.

Decoding the “Why” | What Really Drives US Family Health Insurance Costs?

So, why does your family health insurance monthly cost USA fluctuate, sometimes wildly, year after year? It’s a question I hear all the time, and the answers are multifaceted, rooted deeply in the unique structure of the American healthcare system. First off, we’re not dealing with a single, unified market. Instead, it’s a patchwork of state-specific regulations, regional healthcare costs, and varying competitive landscapes among insurers.

A huge piece of this puzzle is the Affordable Care Act (ACA), often still referred to as Obamacare. Love it or hate it, the ACA fundamentally reshaped how health insurance is priced and offered. Before the ACA, insurers could deny coverage or charge exorbitant rates based on pre-existing conditions. Now, they can’t. This change, while providing crucial protections, also altered the risk pools for insurers, which in turn impacts premiums across the board. The ACA also introduced essential health benefits, meaning all plans must cover certain services, which again, has a cost associated with it.

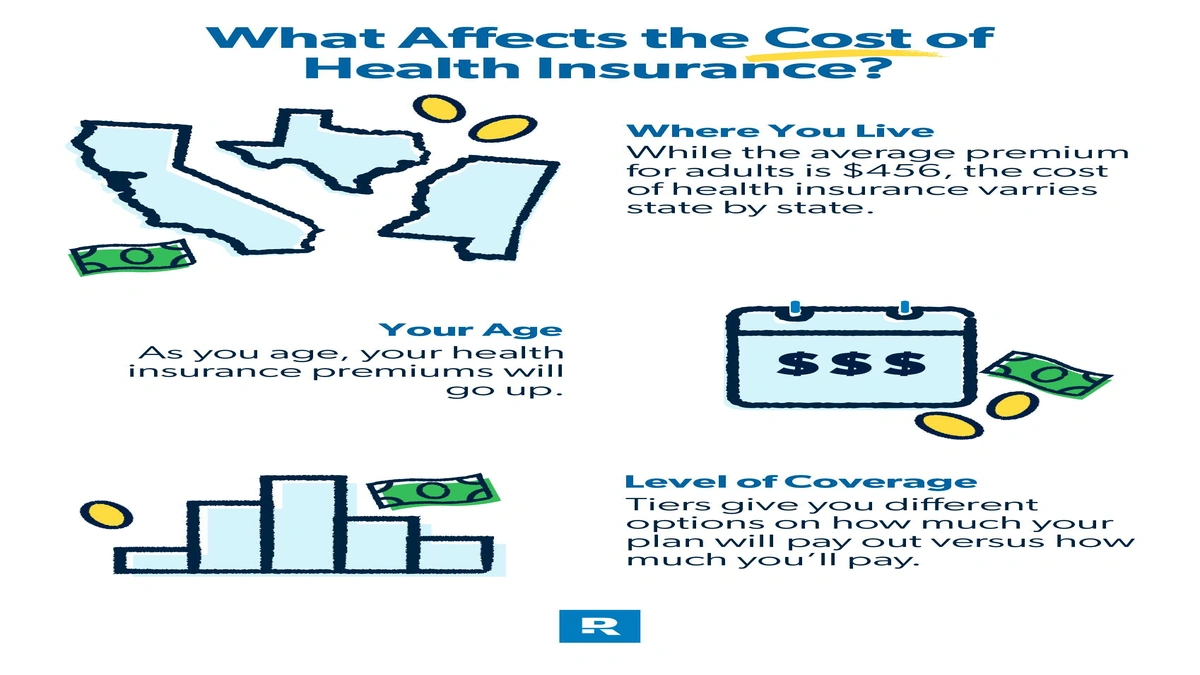

Beyond federal mandates, your personal situation plays a massive role. Factors like the age of family members (older individuals generally cost more to insure), the number of people on your plan, and even your zip code can significantly alter your average health insurance premiums. Healthcare costs vary dramatically from state to state, and even between different counties within the same state. A common mistake I see people make is assuming a plan that’s affordable in one area will be the same elsewhere. It rarely is.

Navigating the Labyrinth | Employer Plans vs. the Marketplace

For many families, the first encounter with health insurance is through an employer-sponsored plan. And let’s be frank, these often seem like the most affordable option. But here’s the thing: while your contribution might be manageable, employers typically subsidize a significant portion of the premium. This hidden subsidy is why employer plans often have lower monthly cost for employees compared to what you’d find on the open market. It’s a huge perk of employment that often goes underappreciated until you lose it.

But what if you’re self-employed, work for a small business that doesn’t offer insurance, or simply prefer to shop around? That’s where the health insurance marketplace (or exchange) comes in. This is the government-run platform (like Healthcare.gov or your state’s equivalent) where individuals and families can purchase plans. This is also where the magic of premium subsidies happens. Based on your household income and family size, you might be eligible for tax credits that significantly reduce your family health insurance monthly cost USA. I’ve seen these subsidies turn what would be an unmanageable premium into something genuinely affordable for many middle-income families.

When comparing individual vs family plans, remember that a family plan isn’t just an individual plan multiplied. Insurers often offer specific family rates that might be more cost-effective than buying separate individual policies, especially if you have multiple children. It’s always worth running the numbers both ways to see which option provides the best value for your specific household composition.

Beyond the Premium | Understanding Your True Out-of-Pocket Expenses

Okay, let’s get real. The premium is just the entry fee. The true cost of healthcare USA extends far beyond that monthly payment. This is where deductibles, copays, coinsurance, and out-of-pocket maximums enter the picture, and understanding them is absolutely critical for understanding your overall financial exposure. A plan with a low premium might look appealing on paper, but if it comes with a sky-high deductible (say, $10,000 for the family), you could be on the hook for a substantial amount of money before your insurance even kicks in for most services.

Think of the deductible as the amount you have to pay out of your own pocket for covered services before your insurance company starts paying. Co-pays are fixed amounts you pay for doctor visits or prescriptions, while coinsurance is a percentage of the cost you pay after your deductible is met. The out-of-pocket maximum is your financial safety net – the absolute most you’ll have to pay for covered services in a plan year. Once you hit that, your insurance pays 100% for the rest of the year.

So, why does this matter so much for your family? Because a low premium plan with a high deductible might be perfect for a young, healthy family who rarely sees a doctor. But for a family with chronic conditions, young children who get sick often, or someone anticipating a surgery, that high deductible could be financially devastating. The key to understanding health plan pricing is to look at the total potential cost: premium + potential out-of-pocket expenses, and choose a plan that aligns with your family’s expected healthcare needs. It’s a bit like assessing the overall cost of running a business; you need to look beyond just the raw material costs and consider all operational expenses, as detailed in guides like this one onsmall business insurance cost.

Smart Strategies for Saving on Health Insurance in the USA

Now that we’ve pulled apart the components of your family health insurance monthly cost USA, let’s talk about action. You’re not powerless here. There are genuine strategies to help you in saving on health insurance.

- Leverage Those Premium Subsidies: If your income falls within 100-400% of the federal poverty level, you are likely eligible for significant premium subsidies through the health insurance marketplace. Don’t assume you earn too much; the income thresholds are more generous than many realize, especially for larger families. Always check your eligibility on Healthcare.gov.

- Consider High-Deductible Health Plans (HDHPs) with HSAs: For healthier families, an HDHP often comes with a lower monthly premium. The real benefit, though, is coupling it with a Health Savings Account (HSA). This allows you to save pre-tax money for medical expenses, and the funds roll over year to year, growing tax-free. It’s a powerful tool for long-term healthcare savings.

- Explore Medicaid and CHIP: For lower-income families, Medicaid (for adults) and the Children’s Health Insurance Program (CHIP) offer comprehensive, low-cost, or even free coverage. Eligibility varies by state, but these programs are lifesavers for millions of families.

- Shop Annually During Open Enrollment: This is perhaps the most crucial tip. Your family’s needs change, and so do the plans available. What was the best plan last year might not be this year. Insurers adjust their offerings, networks, and prices annually. Taking an hour or two during open enrollment to compare plans can yield substantial savings. It’s a bit like how you’d review your home insurance in the UK; different risks, different providers, different costs – the principle of annual review for optimization remains consistent.

- Understand Network Types: HMOs, PPOs, EPOs – these aren’t just acronyms; they dictate your access to doctors and hospitals and impact costs. An HMO might have a lower premium but restrict you to a smaller network, while a PPO offers more flexibility but often at a higher cost. Knowing your family’s preferred doctors and hospitals is key here.

FAQs | Your Burning Questions About Family Health Insurance Costs Answered

What is the average family health insurance monthly cost in the USA?

It’s tough to give a single average because it varies so widely by state, age, family size, and plan type. However, studies from organizations like the Kaiser Family Foundation (KFF) often cite averages for employer-sponsored family plans, which can be over $20,000 annually before employer contributions, meaning an individual’s share might still be several hundred dollars a month. Marketplace plans also vary, but subsidies can drastically reduce the amount you actually pay.

Can I get affordable family health plans if I’m self-employed?

Absolutely! The health insurance marketplace is specifically designed for individuals and families who don’t have access to employer-sponsored insurance. You’ll likely be eligible for premium subsidies based on your income, making coverage much more affordable than the sticker price.

What are deductibles and out-of-pocket maximums, and why do they matter?

Your deductible is the amount you pay for covered services before your insurance starts contributing significantly. The out-of-pocket maximum is the most you’ll pay in a policy year for covered services. Both are crucial because they define your total financial risk. A low premium plan might have a high deductible, meaning you pay more upfront if you need care. Always consider these alongside the premium when evaluating your total US health insurance costs.

How can I reduce my family health insurance monthly cost USA?

The best ways include checking for premium subsidies on the marketplace, comparing plans annually during open enrollment, considering high-deductible plans with HSAs if appropriate for your family’s health, and exploring government programs like Medicaid or CHIP if you qualify. Don’t just stick with your current plan without reviewing options.

What factors affect my health plan pricing besides age and location?

Beyond age and location, family size (more people generally mean higher premiums), tobacco use (insurers can charge more), and the specific plan tier you choose (Bronze, Silver, Gold, Platinum – each with different levels of cost-sharing) all play a role in determining your family health insurance monthly cost USA.

The journey to understanding your family health insurance monthly cost USA is less about finding a magic bullet and more about informed decision-making. It’s about being an active participant in your healthcare choices, not a passive recipient of bills. By understanding the ‘why’ behind the numbers – the market dynamics, the policy implications, and your own family’s unique needs – you gain the power to not just manage, but optimize your healthcare spending. So, take a moment, dig into your options, and empower your family with the knowledge to make the best choices for your health and your wallet. After all, peace of mind is priceless.